When Should You Refinance Your Mortgage?

The break-even math behind refinancing, rate thresholds, and hidden costs most homeowners miss. Use our calculator to see if refinancing pays off.

The Short Answer

Refinance when you can drop your rate by at least 0.75–1%, plan to stay in the home long enough to break even on closing costs, and your credit score hasn't dropped since you bought. For most homeowners in 2026, that means a break-even of 2-4 years.

Break-even happens when cumulative monthly savings exceed closing costs

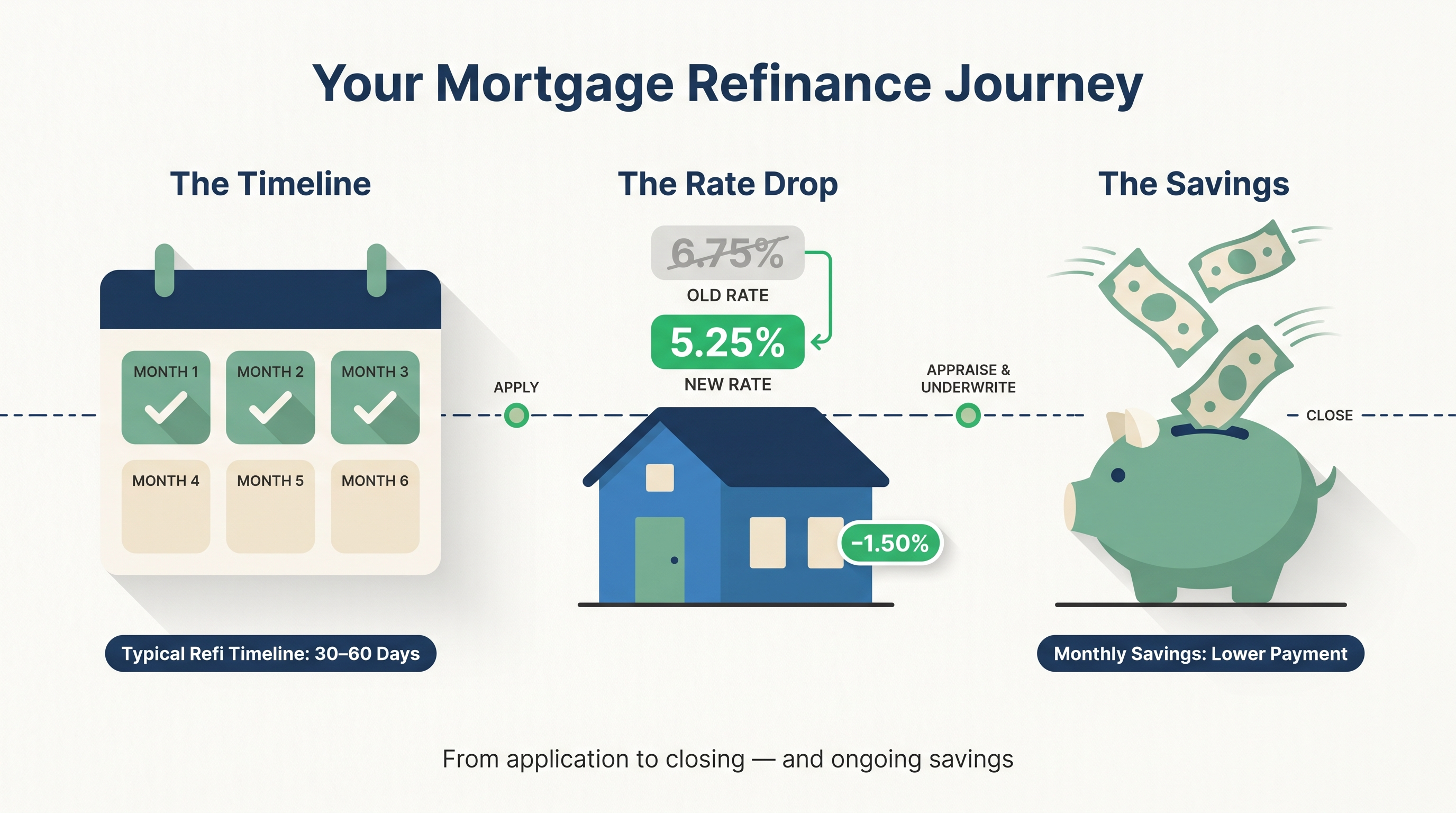

The 2026 Rate Environment

As of mid-2026, mortgage rates have settled into a 5.5%–6.5% range for 30-year fixed loans, down from the 7%+ peaks of 2023 but still elevated compared to the sub-4% era of 2020–2021. This creates a clear opportunity for homeowners who bought or refinanced between 2022 and 2024.

- If your current rate is 7%+: Refinancing is likely worth it. Even a 1% drop saves significant money.

- If your current rate is 6.0%–6.5%: Marginal. Run the numbers carefully — you need a rate drop of at least 0.75%.

- If your current rate is under 5.5%: Probably not worth it unless you need cash out or want to shorten your term.

The Federal Reserve has signaled a slower pace of rate cuts in 2026, so waiting for dramatically lower rates may not pay off. If you can save money now, locking in makes sense rather than timing the market.

The Break-Even Formula

Break-even (months) = Closing costs / Monthly savings

Example for a 2026 refinance:

- Current rate: 7.0%, new rate: 5.75%

- Loan balance: $320,000 (original $400,000, 4 years in)

- Monthly savings: ~$260

- Closing costs: $5,500

- Break-even: 21 months — worth it if you stay 3+ years

Rate Drop Thresholds by Loan Size

The rate drop you need depends on your loan balance. Smaller loans need bigger rate drops to justify closing costs:

| Loan Balance | Min. Rate Drop | Monthly Savings | Break-Even |

|---|---|---|---|

| $150,000 | 1.25% | ~$105 | 38 months |

| $300,000 | 0.75% | ~$190 | 32 months |

| $500,000 | 0.50% | ~$280 | 29 months |

| $750,000 | 0.375% | ~$315 | 29 months |

Types of Refinancing in 2026

Not all refinances are the same. Choose the right one for your goal:

- Rate-and-term refinance: Lower your rate or change your term. Most common in 2026. Best for saving money.

- Cash-out refinance: Borrow against equity. Rates are 0.25–0.5% higher than rate-and-term, but you get cash for renovations or debt payoff.

- Streamline refinance: FHA/VA loans only. Minimal paperwork, no appraisal, faster closing. Popular in 2026 for veterans and first-time buyers.

- No-closing-cost refinance: Lender pays costs in exchange for a slightly higher rate (usually +0.25%). Good if you'll move within 3 years.

How to Shop for Refinance Rates in 2026

Rates vary by 0.5% or more between lenders. Shopping around is the single highest-ROI thing you can do.

- Get 3–5 quotes: Include at least one credit union, one online lender, and one mortgage broker.

- Compare APR, not just rate: APR includes fees. A 5.5% rate with $3,000 in fees may cost more than a 5.75% rate with no fees.

- Check lender reviews: A low rate means nothing if the lender delays closing or adds hidden fees.

- Ask about rate locks: Most lenders offer 30–60 day locks. In a volatile market, lock immediately.

Rate Lock Strategy: When to Lock

In 2026's rate environment, timing your lock matters. Here's the framework:

- Lock immediately if: The rate saves you money and you're happy with it. Rates can rise faster than they fall.

- Float cautiously if: The Fed has just signaled cuts and you're within 2 weeks of closing. Have a backup plan.

- Extended locks: Building a home or refinancing a complex loan? Ask about 90- or 120-day locks (usually costs 0.125–0.25%).

Pro tip: Some lenders offer a "float-down" option — if rates drop after you lock, you can capture the lower rate for a small fee. Ask about this upfront.

Hidden Costs Most People Miss

- Prepayment penalties: Some loans charge 1-3% for paying off early

- Reset amortization: Going from 22 years left to 30 years adds interest

- Cash-out costs: Higher rates and stricter requirements

- Appraisal fees: $400-$600 if your home value dropped

- Title insurance: $500-$1,000 even on a refinance

When NOT to Refinance

- You've had the loan less than 2 years (prepayment penalties)

- Your credit score dropped significantly

- You plan to move within 2 years

- You're almost done paying (last 5-7 years)

Use the Calculator

Our Mortgage Refinance Break-Even Calculatorfactors in closing costs, loan terms, and how long you'll stay to give you a precise answer.

Related Reading

- Should You Pay Extra on Your Mortgage or Invest? — If you're refinancing, should you also pay extra?

- Refinancing on One Income — What to know if your household income has changed.

- Can You Refinance After Losing Your Job? — Options when employment status changes.

- HELOC vs. Cash-Out Refinance — If you need cash, compare these two equity options.

Frequently Asked Questions

Related Articles

Enjoyed This Guide?

Get one homeowner tip per week. No spam, unsubscribe anytime.